The International Monetary Fund (IMF) has stressed the importance of fiscal discipline in Nigeria, particularly in the wake of the country’s ongoing energy subsidy reforms. At a recent briefing in Washington D.C., IMF officials acknowledged Nigeria’s progress in removing the petrol subsidy but emphasized that further reforms were needed to ensure long-term fiscal sustainability. IMF experts, including Davide Furceri from the Fiscal Affairs Department, called for increased domestic revenue generation through tax base expansion and improved spending efficiency to reduce fiscal uncertainty and bolster investor confidence.

The IMF highlighted the broader global economic challenges that Nigeria and other emerging markets face, including rising debt, declining foreign aid, and tightening financial conditions. Era Dabla-Norris, also from the IMF, noted that energy subsidy reforms were crucial for freeing up fiscal resources that could support social spending. However, she cautioned that subsidies were ineffective as a tool for funding social programs and advocated for a phased approach, with targeted support for vulnerable groups to mitigate the social and political impact of these reforms.

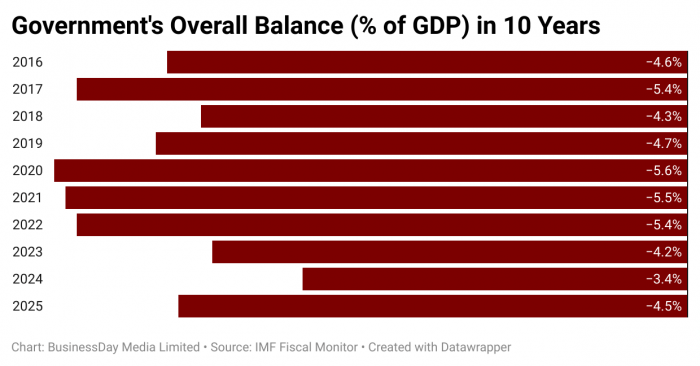

Despite these reforms, the IMF’s projections for Nigeria’s fiscal health remain concerning. The organization forecasted that Nigeria would spend 4.5% more than it earns in 2025, worsening the country’s fiscal deficit. This marks a continued decline in the government’s revenue, projected to fall from 14.4% of GDP in 2024 to just 14% in 2025. The country’s debt-to-GDP ratio is also expected to rise, driven by higher domestic borrowing and exchange rate depreciation, further straining public finances.

The IMF’s concerns are part of a broader warning about the global economic outlook, where rising global debt, trade tensions, and geopolitical uncertainties are threatening fiscal stability worldwide. IMF officials have urged governments to adopt gradual and credible fiscal adjustment plans, especially in low-income and developing nations. They also recommended targeted debt restructuring efforts for countries in distress, warning that without decisive action, global debt could surge to unprecedented levels in the coming years, exacerbating financial instability.

Source: Business day