Nigeria’s journey toward achieving a $1 trillion economy has received cautious recognition from the World Bank, which praised the country’s modest economic improvements while expressing concerns about the sustainability of its ambitious targets. In its latest Nigeria Development Update, the Bank highlighted gains such as rising investor confidence, FX reserve stabilisation, and increased public revenue-to-GDP ratio. However, it warned that reaching the $1 trillion milestone by 2030 would require a fivefold growth acceleration—an uphill task given structural challenges and currency volatility.

The 2025 federal budget, pegged at a record N55 trillion, was a major focal point. While government officials defended the budget as aspirational and growth-driven, the World Bank deemed it “overly ambitious,” warning of revenue shortfalls and potential deficit monetisation. Despite a reduction in fiscal deficit and a notable jump in federation revenues, the report flagged risks of unrealistic projections that could lead to arrears and pressure on public finance. It urged increased transparency, a reduction in the cost of governance, and a shift from symbolic reforms to tangible, productivity-driven strategies.

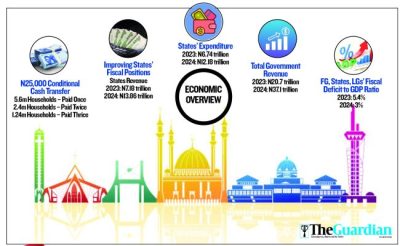

Economic growth for 2024 clocked in at 3.4%, the highest since 2014 (excluding the pandemic rebound), with nominal GDP expanding by 17.1%. However, sustaining this pace would only see Nigeria reach a $1 trillion economy by 2036—not 2030—especially if the naira continues its downward slide. Currency devaluation remains a serious drag on real progress, with over 70% value lost in the last three years. Meanwhile, social safety nets like the conditional cash transfer programme have reached 9.34 million households, but implementation has been uneven and slow.

The Bank commended recent reforms that have led to stronger external positions and fiscal performance, particularly at the state level, where revenue and expenditure more than doubled. Yet, it stressed that Nigeria’s best-performing sectors—like ICT and finance—aren’t translating to broad-based job creation. The report reiterated the need to create more and better jobs at scale, urging a strategy that enables the private sector while investing heavily in public services, infrastructure, and human capital development.

Top government officials responded to the Bank’s assessment by doubling down on their reform agenda. The Finance Minister emphasised the importance of investment in driving job creation and lifting millions out of poverty, while the CBN Governor defended the Bank’s orthodox policy stance, arguing that monetary discipline was necessary for long-term price stability. Meanwhile, telecoms infrastructure development was cited as crucial to strengthening the broader economy, with over $1 billion in investments expected to roll in soon. Ultimately, while the fundamentals show improvement, Nigeria’s path forward still hinges on consistent, inclusive reforms and a stronger grip on inflation and currency stability.