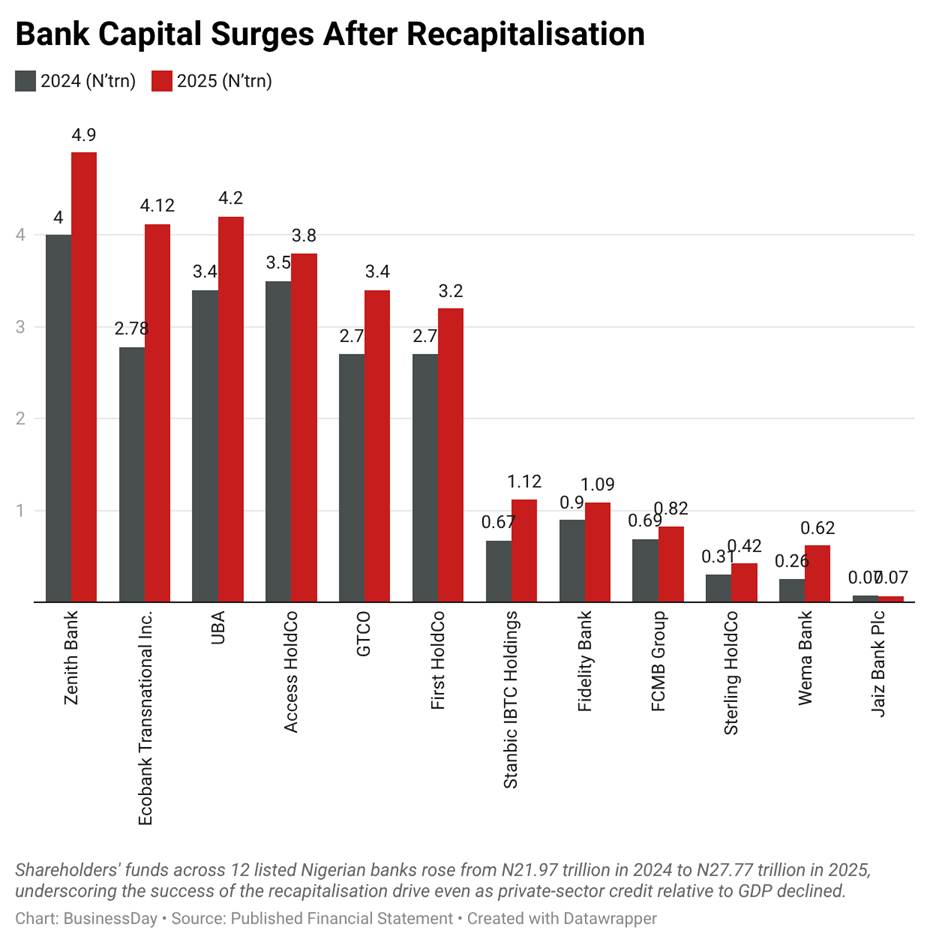

Nigeria’s banking sector is experiencing a remarkable paradox. While banks are stronger and better capitalized than ever before, the flow of credit to businesses is shrinking. Twelve listed banks increased their combined shareholders’ funds from N21.97 trillion in 2024 to N27.77 trillion in 2025, representing a 26.4 percent increase. However, private sector credit as a share of GDP dropped sharply from 33.26 percent to 27.81 percent during the same period, raising concerns about the banking sector’s contribution to economic growth.

The recapitalisation drive introduced by the Central Bank of Nigeria (CBN) in 2024 was designed to create stronger financial institutions capable of supporting large-scale investments and economic expansion. By April 2026, banks had successfully raised more than N4 trillion in fresh capital, improving their resilience against inflationary pressures and currency volatility. Despite these achievements, businesses are seeing little benefit as total private sector credit fell slightly from N76.25 trillion in February 2025 to N75.37 trillion in February 2026.

Experts say the issue is not a shortage of money within the financial system but a growing reluctance to lend to sectors perceived as risky. According to Muda Yusuf, Chief Executive Officer of the Centre for the Promotion of Private Enterprise (CPPE), banks are increasingly favouring industries such as oil and gas and information technology, where returns are higher and risks are lower. With the Monetary Policy Rate standing at 26.5 percent and government securities offering attractive yields, many banks find it safer to invest in treasury instruments than extend loans to manufacturers, farmers and small businesses.

The challenge is particularly severe for small and medium-sized enterprises (SMEs), which contribute nearly half of Nigeria’s GDP and account for more than 80 percent of employment. Despite their critical role in the economy, CPPE estimates show that SMEs receive only about one percent of total bank credit. Analysts also point to lingering bad loans and the high Cash Reserve Ratio imposed by the CBN as factors limiting banks’ ability and willingness to create new loans for productive sectors.

Economists warn that the decline in private sector lending could slow job creation, industrial growth and economic diversification if left unchecked. While recapitalisation has succeeded in strengthening bank balance sheets, experts argue that the next phase of reform must focus on making productive lending more attractive. Improved infrastructure, lower inflation, stronger credit-guarantee schemes and a more stable business environment will be crucial if Nigeria hopes to translate stronger banks into stronger economic growth. For now, the country’s banking sector may be growing bigger, but its impact on the real economy remains a work in progress.

source: Businessday