The world’s biggest currency banks see the dollar edging lower toward year-end, a consensus that may only hold if rising coronavirus infections don’t hamper the global growth rebound.

Among the banks that handle the brunt of the $6.6 trillion in daily foreign-exchange turnover, the median forecast is for the greenback to fall nearly 2% against the euro and 3% against the yen in the next six months. Key to that view is the gradual unwinding of the haven demand that fueled a dollar surge in March as investors sought safety with the world’s economy grinding to a halt.

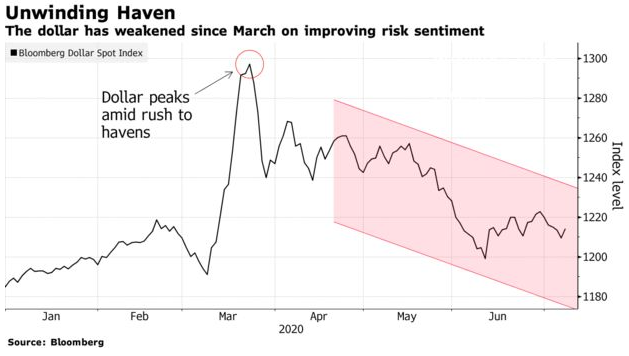

So far, the playbook is working. The Bloomberg dollar index is down about 7% from its March peak as business activity recovers across major economies and stocks rebound. However, for strategists with the unenviable task of projecting exchange rates now — with the world’s biggest economy rebounding but at a perilous stage in terms of the virus — the best approach may be to avoid getting bogged down in attempting to forecast the path of the disease.

“We’re probably better economists than epidemiologists,” Vassili Serebriakov, a strategist at UBS Group AG, said in an interview. “The dollar tends to weaken in this phase of the growth cycle,” when the global economy transitions from recession to recovery, he said.

For the most part, the 11 banks surveyed are only calling for modest shifts in exchange rates, a stance that may come in part from the complexity of the period ahead.

The median forecast for the euro at year-end is $1.15, not much higher than the spot level of about $1.13. Two banks have it dropping to $1.10 or below by year-end, and only one sees it advancing beyond $1.16. For the yen, the median of 104 per dollar by the end of the fourth quarter represents a modest appreciation from the current level of around 107. While three banks see it at 100 by 2021, none expect it to weaken past 110.

Of course, forecasting is a challenge now across financial markets. Citigroup Inc.’s economic surprise index for U.S. indicators has never been higher. And in stocks, many companies are declining to provide guidance on earnings.

For currency strategists plotting out the relative strengths of world economies, the virus is far from the only wild card in the pipeline.

The U.S. presidential vote is less than four months off, with Democratic nominee Joe Biden now odds on to take the White House. Some analysts point to historical patterns suggesting the greenback is poised to gain regardless of who wins. Others anticipate that a Biden victory would lead to tax hikes on corporations that would hurt stocks first and the dollar second.

State Street Corp. sees a Democratic White House as bearish for the dollar, particularly if the party also takes the Senate.

“Any Biden presidency is unlikely to be as Wall Street-friendly as that of Trump and the uncertainty at least is likely to curb capital inflows to the U.S. as the election nears,” said Lee Ferridge, head of macro strategy.

New Europe

While most analysts were focused on the dollar, some see the European Commission’s plan to issue mutualized debt as positive for the euro. The shared bonds are considered a significant, if tentative step toward a fiscal union, which could ease the existential threat that has plagued the common currency over the past decade.

Decisive action from the European Central Bank, together “with the strong push by Germany and France for a common fiscal response,” means that “the days where euro zone policy makers were seen lagging whenever a meaningful response was required now seem a more distant memory,” said Ferridge at State Street.

The plan is still far from finalized though. Four EU countries — Austria, Denmark, the Netherlands and Sweden — oppose handouts to the hardest-hit nations, and are set to release their own version likely to be based on loans. A watered-down approach could weigh on the common currency.

Bank of America Corp. was the most bearish on the euro among those surveyed, expecting $1.05 at the end of the year, partly because of what it sees as weaknesses in the region’s fiscal plans.

“There is still work to do in terms of how much fiscal stimulus will be needed for the European economy,” the bank’s strategists wrote in a June 25 note.

On the monetary front, “relative central bank action” may also depress the euro. “Fed action has been historic, but the expansion of the Fed balance sheet may have run most of its course” compared with the ECB, they continued.

Haven Lure

That won’t help against the yen, though. The Fed’s deep rate cuts in response to the pandemic trimmed the rate differentials between the two economies. And with the Fed signaling little chance of a hike through 2022, the greenback’s long-held yield advantage over Japan’s currency may struggle to recover.

“The best predictor of dollar-yen behavior is 10-year real rate differentials between the U.S. and Japan,” said Serebriakov at UBS. “Because real rates in the U.S. have collapsed, that particular metric would point to a much lower dollar-yen.”

Still, there’s scope for yen weakness. While the country has mostly kept the virus in check, its economy has taken a battering nonetheless, leading to a massive stimulus package. Citigroup, the most bearish on the yen, is calling for 110 per dollar by the end of the year because it expects the effort could disappoint.

That may not be significant if the pandemic starts shuttering activity again around the world, a gloomy prospect that would spark another round of flight to safety, favoring refuges like the dollar and the yen.

David Bloom, HSBC Holdings Plc’s global head of currency strategy, is leaning toward haven currencies for that reason, expecting the yen to strengthen to 105 by the end of December.

“We’re very cautious on the bounce-back, so defensive currencies will do quite well,” he said. “In a world of uncertainty, a problematic world, we’ve got a slightly stronger yen.”

| EUR/USD FORECAST | END-Q3 | END-Q4 |

|---|---|---|

| Bank of America | 1.08 | 1.05 |

| Barclays | 1.16 | 1.16 |

| BNP Paribas | 1.10 | 1.12 |

| Citigroup | 1.14 | 1.16 |

| Deutsche | 1.12 | 1.15 |

| Goldman Sachs | 1.12 | 1.15 |

| HSBC | 1.10 | 1.10 |

| JPMorgan | 1.13 | 1.11 |

| Standard Chartered | 1.13 | 1.16 |

| State Street* | – | 1.20 |

| UBS | – | 1.15 |

| * Second half view |

— Bloomberg