Stocks could be volatile in week ahead amid turbulence from cryptocurrency

The plunge in bitcoin helped sour the mood for all risk assets, though the tech sector eked out a small gain for the past week. The Fed’s preferred inflation measure, the personal consumption expenditures price index, will be released Friday. That report could affect the market if the number is hot. Earnings season is slowing down, but there are still some important companies, like Costco and NVIDIA, releasing reports.

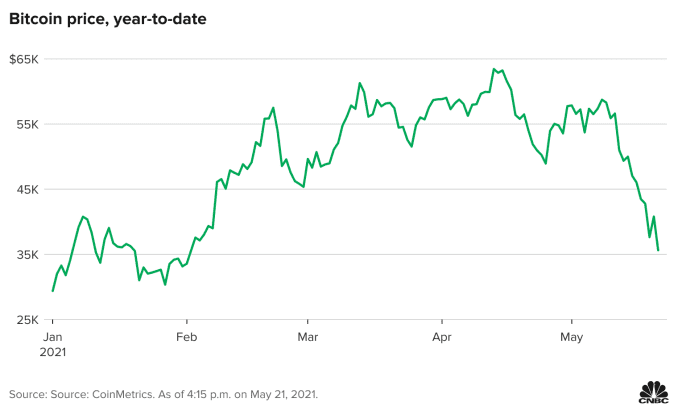

The trading pattern of the past two weeks – particularly alongside cryptocurrency’s movements – suggests stocks could continue to be volatile in the week ahead.

Investors are watching the wild swings in bitcoin and trying to gauge whether technology shares can gain traction after a rally attempt in the past week.

A steep plunge in bitcoin after China announced new regulations soured the mood for risk assets during the past week. The U.S. also called for stricter compliance with the IRS. Further, on Friday, China said it would crack down on bitcoin mining and trading.

“What’s interesting is the market is being bullied around by where bitcoin goes,” said Peter Boockvar, chief investment officer with Bleakley Advisory Group. Bitcoin plunged by as much as 30% on Wednesday, to about $30,000. Though it recovered to above $42,000, it slid again on Friday.

The cryptocurrency was down about 9% late Friday, hovering around $36,000, according to Coin Metrics.

“Bitcoin is a poster child for risk appetite,” said Boockvar. “It tells you the stock market is more on uneven ground, if we’re getting dragged along by bitcoin.”

There is some key data in the week ahead. Consumer confidence, home price data and new home sales are out on Tuesday. Durable goods will be released Thursday, and the consumer sentiment report is issued Friday.

There is some key data in the week ahead. Consumer confidence, home price data and new home sales are out on Tuesday. Durable goods will be released Thursday, and the consumer sentiment report is issued Friday.But the most important data will be the personal income and spending data, which includes the personal consumption expenditure price deflator, the Fed’s preferred inflation measure.

“The key to next week is going to be the inflation numbers. The inflation numbers are now becoming the new payroll numbers in terms of market performance,” said Boockvar. “What will also be interesting is inside the consumer confidence numbers, is where the inflation expectations go.”

The consumer price index was surprisingly hot when released last week, showing core inflation at a year over year pace of 3% in April. The core PCE price index was up 1.8% year over year in March.

In the week ahead, earnings season is winding down but there continue to be reports from retailers, like Best Buy, Costco and Nordstrom. NVIDIA and Dell also report.

No correction yet

As the market has chopped around this month, dip buyers have stepped into the declines and snapped up perceived bargains.

Some strategists do not see a correction just yet, though pullbacks could continue.

“For me, my framework is we can only get a 10% correction when we have a liquidity set back, when we have a policy tightening,” said Barry Knapp, managing partner of Ironsides Macroeconomics. “In any of the little disturbances, we are getting about a 4% to 6% pullback.

Knapp said investors are fretting too much about higher interest rates being a problem for technology companies. “You should be in the cyclical parts of tech,” he said. Knapp noted that subsectors like semiconductors and software should do well with the economic reopening and global manufacturing rebound.

Tech squeaked out a slight gain in the past week, gaining 0.1%, but semiconductors popped nearly 3%. Software was up 0.2%.

The Nasdaq was 0.3% higher on the week to 13,470, while the Dow was off a half percent at 34,207. The S&P 500 was down 0.4% to 4,155.

The best performing sector was real estate investment trusts, up 0.9%, followed by health care, up 0.7%. Biotech was higher on the week with the IBB iShares Nasdaq Biotech ETF, up 1.1%.

“It wouldn’t shock me if we went straight back to new highs,” Knapp said. “Part of the reason I thought we would trade in a range, was earnings season was done but net revisions is surging.”

He said earnings for the S&P 500 are now expected to be up 7% more for the year than when the first quarter reporting season began.

Knapp expects the Fed may discuss tapering its bond buying at its Jackson Hole meeting in late summer, and that is the likely trigger for a correction. Back to World War II, he said the first correction after a recession was triggered by the Fed normalizing policy.

“Last cycle, we had eight of those,” he said. “Every attempt they made to normalize policy caused one of these risk off events.”

Knapp said it’s natural for investors to be focused on the Fed now. “It’s an uncertainty shock,” he said. “It will cause a correction and everyone is focused on it. The Fed has not really changed its policy since the depths of the pandemic.”

Knapp said Treasury yields have drifted lower during efforts in Washington to reach a bipartisan plan on infrastructure spending. But he expects the market to react differently in the next two weeks, since he expects those efforts will clearly fail and Democrats will focus on a big spending program that will increase the deficit.

The bitcoin crypto mania was lifted by the idea of big spending from Washington, and the infrastructure spending could be positive. “The thing that was the surprise in 2021 that really drove the mania was the blue wave and then the spending blowout,” he said, noting bitcoin gained on the potential for inflation and big deficit spending.

Week ahead calendar

Monday

Earnings: Lordstown Motors

12:00 p.m. Atlanta Fed President Raphael Bostic

5:30 p.m. Kansas City Fed President Esther George

Tuesday

Earnings: Nordstrom, Toll Brothers, Intuit, Agilent, Autozone, Cracker Barrel, Pershing Square Holdings, Urban Outfitters, Zscaler

9:00 a.m. S&P/Case-Shiller home prices

9:00 a.m. FHFA home prices

10:00 a.m. New home sales

10:00 a.m. Consumer confidence

10:00 a.m. Fed Vice Chairman Randal Quarles at Senate Banking Committee

Wednesday

Earnings: NVIDIA, Snowflake, Bank of Montreal, Capri Holdings, Abercrombie and Fitch, Dick’s Sporting Goods, American Eagle Outfitters, Workday, Pure Storage, Designer Brands

3:30 p.m. Fed Vice Chairman Quarles

Thursday

Earnings: Best Buy, Salesforce.com, Costco, Dell Technologies, Box, Ulta Beauty, VMWare, Autodesk, Lions Gate, Canadian Imperial Bank, Toronto Dominion, Burlington Stores, Dollar General, Dollar Tree, Royal Bank of Canada, Medtronic

8:30 a.m. Initial jobless claims

8:30 a.m. Durable goods

8:30 a.m. Real Q1 GDP

10:00 a.m. Pending home sales

Friday

8:30 a.m. Personal spending (PCE deflator)

8:30 a.m. Advance indicators

9:45 a.m. Chicago PMI

10:00 a.m. Consumer sentiment

– CNBC